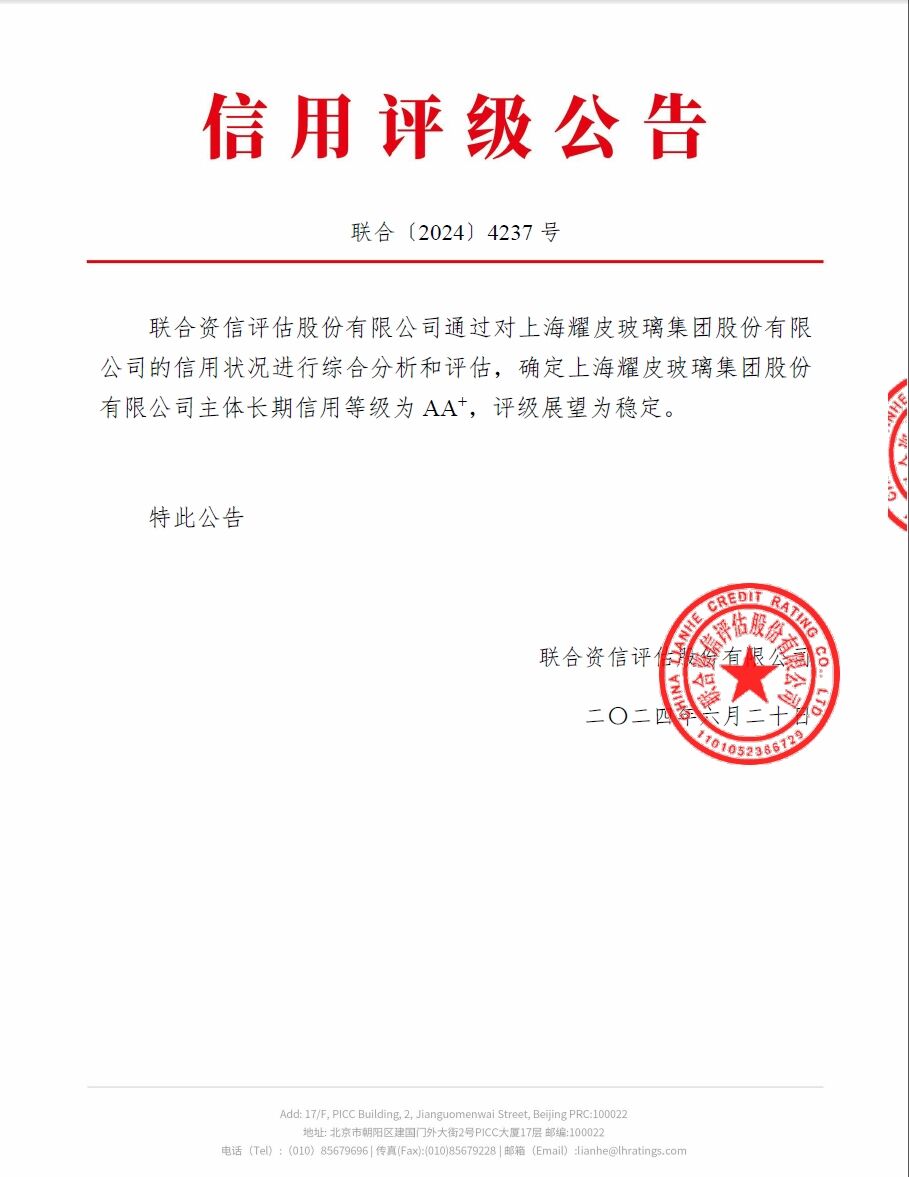

On June 20, 2024, United Credit Appraisal Co., Ltd. conducted a comprehensive analysis and evaluation of the credit status of Shanghai Yaopi Glass Group Corporation (hereinafter referred to as the “Company”) and issued a credit rating report, which determined that the main body of Shanghai Yaopi Glass Group Corporation has a long-term credit rating of AA+, and the outlook of the rating is stable. The rating outlook is stable.

In 2023, the world economy is in the doldrums, geopolitical conflicts are complicated and volatile, and China's macro policy seeks progress while stabilizing and strengthens counter-cyclical regulation and control. As for the downstream industries closely related to the Company's development, the domestic real estate market continued to bottom out in 2023, with the area of new construction declining by 20.4% year-on-year, and the demand for glass continued to weaken. Automotive industry, the wave of price cuts to promote the slow recovery of the automotive industry, and in the national and local policies to help, the domestic auto market demand continues to release, coupled with the continuation of the strong momentum of automotive exports, the annual automotive production and sales increased by 11.6% year-on-year growth of 11.6% and 12.0%, a record high. The high-speed development of new energy vehicles and the structural adjustment between new energy vehicles and traditional fuel vehicles provide challenges and opportunities for the company.

“Ideas determine the way out, innovation creates the future” is the core driving force of the Group's continuous exploration of transformation and development. Against the backdrop of many uncertainties in the domestic and international situations, the Group made targeted efforts, pressurized and advanced, responded to changes scientifically and proactively, and actively coordinated the production and operation of the three major business segments. The float glass segment has adjusted its product structure and taken various measures to reduce the procurement cost of raw fuels, and has achieved stable and high production of high value-added products such as Auto Low-e online coated glass for automobile sunroofs, online coated TCO glass for solar thin film power generation, and CSP glass for photovoltaic solar energy; the architectural glass segment has continued to improve the production of BIPV power generation curtain wall glass combined with the TCO substrate produced by Dalian Yaopi, and the super energy-saving glass combined with offline glass. The architectural glass segment continued to increase the sales proportion of special deep-processed products combining energy-saving and energy-creation, such as BIPV power generation curtain wall glass with TCO substrate produced by Dalian Yaopi, and online and offline super energy-saving glass, etc. The automotive glass segment deepened the adjustment of the product structure, expanded the sales proportion of canopy and sunroof with Auto Low-e online coated glass produced by Dalian Yaopi, and comprehensively expanded the overall cooperation with NSG in the field of automotive OE and AGR. In the first half of the year, the Company achieved an overall operating income of RMB2.75 billion, an increase of 14.8% over the same period of the previous year; total profit of RMB82.25 million; and net cash flow of RMB259 million, an increase of RMB246 million over the same period of the previous year.

The credit rating work has been fully supported by the Group's leaders and actively cooperated by the Group's departments and subsidiaries. From the sorting of interview outline questions in the early stage of the rating work, on-site and video interviews and factory research conducted by the rating agency, to the collection and collation of a large amount of information in the middle of the rating, to the feedback of the initial credit enhancement information in the late stage of the rating, the feedback of the first trial and the feedback of the second trial, the Group's Finance Department combined with the main contents of the interviews of the executives to communicate repeatedly with the rating agency based on the aspects of operation and management, risk control, technical level and financial situation to elaborate the The company's development philosophy and confidence in the company's development were finally reviewed and approved by the Joint Credit Review Board, which determined that the company's main long-term credit rating is AA+, and the rating outlook is stable.

The main long-term credit rating of AA+ and stable rating outlook is not only a comprehensive affirmation of the company's comprehensive strength, but also conducive to the company's further reduction of financing costs, broadening of financing channels, enhancement of financing capacity, optimization of the financing structure, and at the same time, enhance the company's brand reputation and market competitiveness, and escort the company's future development.

Hot News

Hot News2025-12-19

2025-07-10

2025-06-11

2025-05-08

2025-05-08

2025-02-25

Copyright © 2026 China Shanghai Yaohua Pilkington Glass Group Co., Ltd. All Rights Reserved. Privacy policy